Big news this week. Green beans are extremely tight on both coasts, and prices are being pushed to a ten-year high. The Mother’s Day pull is keeping the demand up.

Did you think we were going to write the same intro that’s in every other Monday newsletter?

ProduceIQ Index:$1.07/pound, up -4.5 percent over prior week

Week #18, ending May 5th

Blue Book has teamed with ProduceIQ BB #:368175 to bring the ProduceIQ Index to its readers. The index provides a produce industry price benchmark using 40 top commodities to provide data for decision making.

This is a post-coronation edition, after all, and we are not above attempting to incorporate the peripheral headlines. Especially the ones about all the really old and extremely rich dudes that are saturating trending charts, all in the name of SEO, of course. (Looking at you, King Charles the III, and the capitalist equivalent of royalty: Warren Buffet and Charlie Munger)

But At $34, bean prices are the only kings that have us concerned this week (well, perhaps grapes and celery as well).

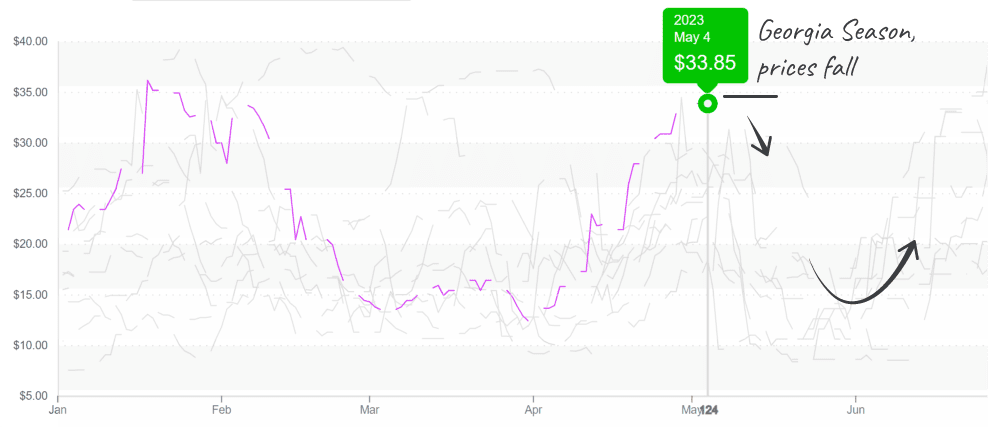

In the West, supply is forecasted to tighten for 1-2 weeks. In the East, Florida’s acreage has been low, and the season is winding down production earlier than anticipated due to intense wet weather throughout the Southeast. Georgia is a couple of weeks out from filling the remaining Eastern supply gap.

Green beans exceed $30 and may remain high for longer than usual.

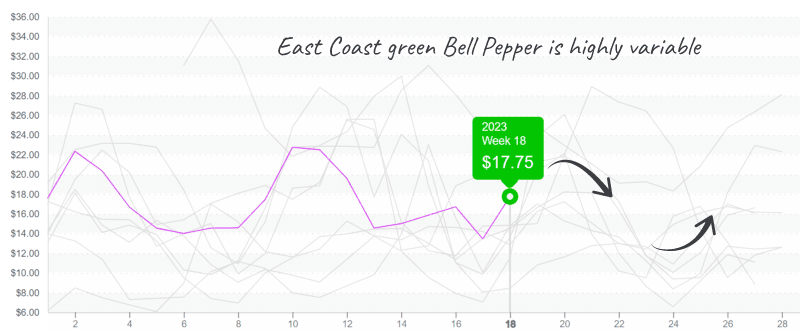

Wild weather in the Southeast isn’t just affecting green bean markets. Bell peppers, up +15 percent, to $18, over the previous week, are rising in anticipation of tightening green and colored supply.

Thanks to steady supply and multiple online growing regions in the West, markets are coping with struggling Eastern supply uncharacteristically well. As a result, eastern quality could be better but will improve as Georgia growers come online.

Green bell pepper in the East has remained volatile through the Georgia season over the past ten years.

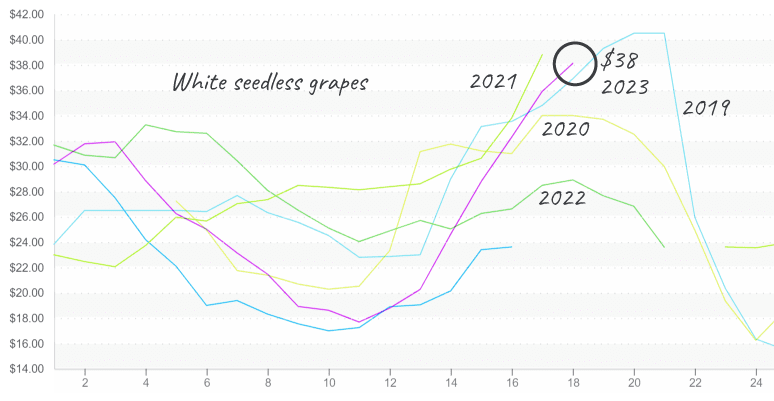

Week #18 red and green grapes are fetching a kingly price. It’s not that there are absolutely no grapes, but outside of 2020, USDA reported volume has never been this low in the last ten years.

For context, an annual supply gap exists between weeks #15 and #20 as production moves from South America to Mexico. But this year, Chile’s early and dramatic end to their Spring export season and Mexico’s delayed start are forcing prices to a shocking $33.

Unlike a real shortage, suppliers won’t feel the effects simultaneously. Still, they will most likely experience severe volatility in product availability as buyers look to fill gaps in the spot market. Moreover, because of the severity of the shortage, conditions are expected to persist through May and into June.

Table grapes are reacting as anticipated for seasonal shortage.

Good news, grapes may be in dismal form for the most sacred of all holidays, but strawberry markets are in great shape for Mother’s Day next week. Excellent quality and strong availability are keeping prices in line with the USDA average—a solid opportunity to promote for dads and kids hoping to surprise mom with a special holiday breakfast.

In line with last week’s predictions, celery prices are rising rapidly. Prices are up +63 percent over the previous week and are poised to climb higher. Waning supply in Santa Maria/Oxnard, CA, combined with unseasonably wet and cool weather, leads to tighter supply.

Expect instability over the next two weeks as growers in Watsonville, CA, ramp up production.

The ProduceIQ Index is the fresh produce industry’s only shipping point price index. It represents the industry-wide price per pound at the location of packing for domestic produce, and at the port of U.S. entry for imported produce.

ProduceIQ uses 40 top commodities to represent the industry. The Index weights each commodity dynamically, by season, as a function of the weekly 5-year rolling average Sales. Sales are calculated using the USDA’s Agricultural Marketing Service for movement and price data. The Index serves as a fair benchmark for industry price performance.

Big news this week. Green beans are extremely tight on both coasts, and prices are being pushed to a ten-year high. The Mother’s Day pull is keeping the demand up.

Did you think we were going to write the same intro that’s in every other Monday newsletter?

ProduceIQ Index:$1.07/pound, up -4.5 percent over prior week

Week #18, ending May 5th

Blue Book has teamed with ProduceIQ BB #:368175 to bring the ProduceIQ Index to its readers. The index provides a produce industry price benchmark using 40 top commodities to provide data for decision making.

This is a post-coronation edition, after all, and we are not above attempting to incorporate the peripheral headlines. Especially the ones about all the really old and extremely rich dudes that are saturating trending charts, all in the name of SEO, of course. (Looking at you, King Charles the III, and the capitalist equivalent of royalty: Warren Buffet and Charlie Munger)

But At $34, bean prices are the only kings that have us concerned this week (well, perhaps grapes and celery as well).

In the West, supply is forecasted to tighten for 1-2 weeks. In the East, Florida’s acreage has been low, and the season is winding down production earlier than anticipated due to intense wet weather throughout the Southeast. Georgia is a couple of weeks out from filling the remaining Eastern supply gap.

Green beans exceed $30 and may remain high for longer than usual.

Wild weather in the Southeast isn’t just affecting green bean markets. Bell peppers, up +15 percent, to $18, over the previous week, are rising in anticipation of tightening green and colored supply.

Thanks to steady supply and multiple online growing regions in the West, markets are coping with struggling Eastern supply uncharacteristically well. As a result, eastern quality could be better but will improve as Georgia growers come online.

Green bell pepper in the East has remained volatile through the Georgia season over the past ten years.

Week #18 red and green grapes are fetching a kingly price. It’s not that there are absolutely no grapes, but outside of 2020, USDA reported volume has never been this low in the last ten years.

For context, an annual supply gap exists between weeks #15 and #20 as production moves from South America to Mexico. But this year, Chile’s early and dramatic end to their Spring export season and Mexico’s delayed start are forcing prices to a shocking $33.

Unlike a real shortage, suppliers won’t feel the effects simultaneously. Still, they will most likely experience severe volatility in product availability as buyers look to fill gaps in the spot market. Moreover, because of the severity of the shortage, conditions are expected to persist through May and into June.

Table grapes are reacting as anticipated for seasonal shortage.

Good news, grapes may be in dismal form for the most sacred of all holidays, but strawberry markets are in great shape for Mother’s Day next week. Excellent quality and strong availability are keeping prices in line with the USDA average—a solid opportunity to promote for dads and kids hoping to surprise mom with a special holiday breakfast.

In line with last week’s predictions, celery prices are rising rapidly. Prices are up +63 percent over the previous week and are poised to climb higher. Waning supply in Santa Maria/Oxnard, CA, combined with unseasonably wet and cool weather, leads to tighter supply.

Expect instability over the next two weeks as growers in Watsonville, CA, ramp up production.

The ProduceIQ Index is the fresh produce industry’s only shipping point price index. It represents the industry-wide price per pound at the location of packing for domestic produce, and at the port of U.S. entry for imported produce.

ProduceIQ uses 40 top commodities to represent the industry. The Index weights each commodity dynamically, by season, as a function of the weekly 5-year rolling average Sales. Sales are calculated using the USDA’s Agricultural Marketing Service for movement and price data. The Index serves as a fair benchmark for industry price performance.

Mark Campbell was introduced to the fresh produce industry as a lender for Farm Credit. After earning his MBA from Columbia Business School, he spent seven years as CFO for J&J Family of Farms and later served as CFO advisor to several produce growers, shippers, and distributors. In this role, Mark saw the impediments that prevent produce growers and buyers to trade with greater access and efficiency. This led him to cofound ProduceIQ.